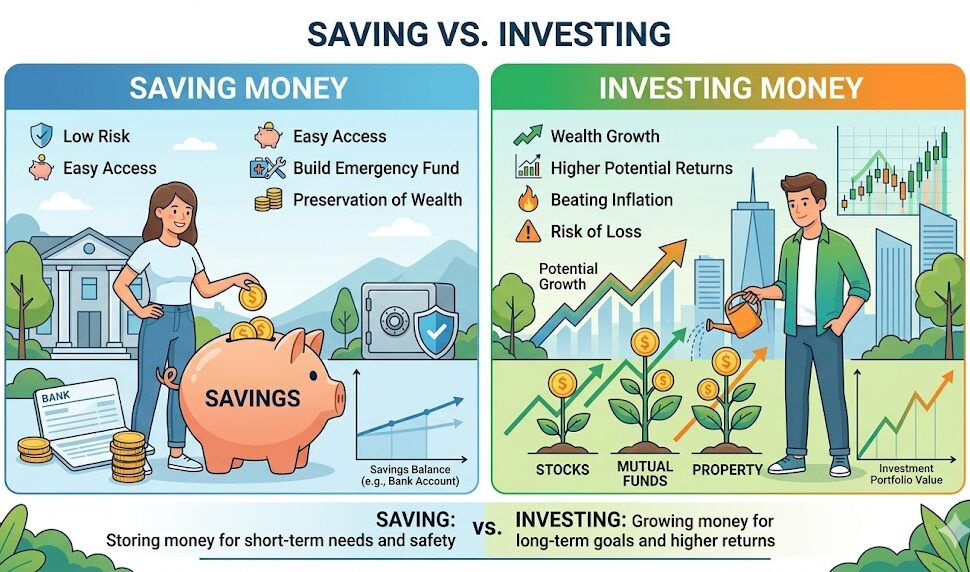

Saving money is a financial practice that entails allocating a portion of income for future use. This can be achieved through various methods, with savings accounts being one of the most common options. A savings account is typically offered by banks or credit unions and allows individuals to deposit money, which can earn interest over time. One of the defining characteristics of savings is its emphasis on safety; funds deposited in savings accounts are generally insured, providing a sense of security for account holders.

Liquidity is another vital aspect of saving. Saving money accounts offer easy access to funds, allowing individuals to withdraw their money as needed without significant penalties. This makes them particularly well-suited for short-term financial goals, such as building an emergency fund, making a purchase, or saving for a vacation. In times of unexpected events, having adequate savings can be crucial for financial stability and help prevent debt accumulation.

Establishing an emergency fund is an essential part of sound financial planning. This fund is an amount set aside exclusively for unforeseen circumstances, such as medical emergencies or sudden job loss. Financial experts typically recommend having at least three to six months’ worth of living expenses readily available in an emergency fund. By prioritizing saving, individuals can create a safety net that alleviates financial stress during emergencies.

In summary, saving is an integral component of personal finance that focuses on securing resources for short-term needs while building a safety net for the future. Through reliable savings accounts, individuals can safely earn interest on their funds while ensuring they have liquidity to access money whenever necessary.

Understanding Investing

Investing refers to the strategic allocation of funds into various assets, such as stocks, bonds, or real estate, with the objective of generating a return over time. The primary goal of investing is to grow wealth and build financial security, often through long-term capital appreciation. Unlike saving, which typically prioritizes preserving capital, investing embraces a certain level of risk, acknowledging that higher potential returns can often come with increased volatility.

There are several types of investments available, including equities, fixed income instruments, and property. Equities, or stocks, represent ownership in a company, and their value can fluctuate based on the company’s performance and market conditions. Fixed income investments, such as bonds, offer more stable returns by paying interest over time. Real estate can provide both rental income and appreciation in value. Each investment type comes with its own risk profile, and an investor’s choice may depend on their risk tolerance and investment horizon.

One critical factor in investing is the concept of compound interest, which refers to earning returns on both the initial principal and the accumulated returns from previous periods. This effect can significantly amplify the growth of an investment over the long term, making it a vital component of effective investing strategies. However, it is essential to be mindful of market fluctuations as these can directly impact investment values. Understanding the market’s cyclical nature and having patience during downturns is crucial for successful investing.

By embracing the long-term objectives of investing, individuals can potentially achieve financial goals that exceed mere preservation of capital, ultimately inviting a more prosperous future.

Key Differences Between Saving and Investing

When considering the financial landscape, it is imperative to understand the distinctions between saving and investing, as these concepts play vital roles in managing personal finances. The primary difference lies in the level of risk involved. Saving is often associated with low-risk financial instruments such as savings accounts or certificates of deposit, which offer limited returns. The focus here is on preserving capital, making it suitable for short-term financial goals or emergencies.

Conversely, investing typically entails a higher degree of risk but presents opportunities for greater returns over time. Investments may include stocks, bonds, real estate, or mutual funds, all of which are subject to market fluctuations. As a result, investors face the possibility of losing part or all of their principal investment, but they also have the potential for significant capital appreciation and income generation.

The time horizon is another critical factor differentiating saving from investing. Saving money is generally short-term, addressing immediate financial needs like building an emergency fund or fulfilling short-term expenses. In contrast, investing is oriented toward long-term financial goals, such as retirement or wealth accumulation, necessitating a longer time commitment to weather market volatility.

Liquidity is also an essential consideration. Saving money are typically liquid, allowing easy access to funds without penalties, making them ideal for urgent needs. However, investments may not be as liquid; they often require time to convert to cash without incurring significant losses. Knowing when to save versus when to invest can guide individuals in aligning their financial strategies with their specific goals, whether it is preserving capital or pursuing higher returns.

When to Save vs. When to Invest

Deciding whether to save or invest can significantly influence your financial stability and growth. The choice largely depends on your individual circumstances, including your age, financial goals, risk tolerance, and current market conditions. Understanding when to save versus when to invest is crucial for making sound financial decisions.

Generally, Saving money is advisable when you need to secure funds for short-term goals or emergencies. For instance, if you are planning to purchase a home within a couple of years, allocating funds in a high-yield savings account can ensure that your down payment remains safely accessible. Additionally, having an emergency fund—typically covering three to six months of expenses—is crucial to protect against unforeseen events, thereby reinforcing the importance of saving.

Conversely, investing is more beneficial for long-term financial objectives. Individuals in their 30s or 40s might prioritize investing for retirement or wealth accumulation. Stocks and mutual funds, for example, provide the potential for higher returns over extended periods, compensating for the inherent risks that come with market fluctuations. For those comfortable with a degree of volatility and who have a substantial investment timeline, engaging in a diversified investment portfolio can yield significant benefits.

Assessing your risk tolerance is another critical factor in determining when to save or invest. Younger individuals typically have a higher risk appetite, allowing them to leverage investment opportunities more aggressively. In contrast, those nearing retirement might favor stable savings options, as they seek to preserve their capital.

Ultimately, a balanced approach that includes both saving and investing is recommended for comprehensive financial health. Establishing clear financial goals will enable you to craft a strategy that encompasses both elements, ensuring you are prepared for both immediate needs and future aspirations.